Techsurance - your weekly insurance technology readings🗞

19 July - 09 August - Episode 1

Hi everyone,

I skipped the last three weeks’ Insurtech Insights (apologies! 🙈), so am catching up this week with two longer editions before going on holidays 🛫🛬. This is the first newsletter of a (short) series of two, so stay tuned for more Insurtech news.

And don’t forget to subscribe if you like the content 😎

📗 Plenty of insights from the industry this week

Willis Tower Watson released its Quarterly Insurtech Briefing for Q2’2021. Link to the full briefing here 📰 Willis Tower Watson. Here are some key highlights from Q2:

Insurtechs raised a record-breaking $7.3 billion in H1’2021, already surpassing the amount raised during the whole of 2020.

This record-breaking funding quarter was fuelled by megarounds (think Wefox, Bought By Many, or Shift Technologies and Alan in France). Collectively, the 15 funding rounds represented nearly $3.3 billion or 67% of total funding.

Early- and mid-stage Insurtechs deals remains healthy. Deal activity was driven by mid-stage (Series B and C) deal share, which increased by 6% to 23%.

Geographic diversity among global InsurTechs continues to grow, with InsurTechs from 35 distinct countries securing investments, compared with 26 countries in Q1 2021.

InsurTechs focused on distribution accounted for nearly 55% of all deal activity, a 7% increase from last quarter.

Market conditions are tightening for Insurtechs that went public. Furthermore, the latter tend to have underperformed on the stock market.

The German insurance watchdog forecasts €5.5bn worth of flood damage claims. The flooding, near Cologne and Bavaria, collapsed houses, washed away cars and left people stranded on rooftops. Some 40,000 vehicles were damaged or destroyed. While at least 180 people were killed 📰 Insurtech Insights

2021’s extreme weather leads to insurers’ biggest payout in 10 years. Aon estimates that global natural disaster insured losses, the amount insurers are forecast to pay out, will be as high as $42bn (£31bn) for the six-month period 📰 The Guardian

Global insurance recovery will be faster, stronger than in 2008, according to Swiss Re. Swiss Re said it expects annual growth for all premiums, not just commercial, to reach 3.3% this year and 3.9% in 2022, after falling just 1.3% last year. That compares with a 3.7% decline in 2008, during the financial crisis, and a slower rebound of 0.5% and 2.1% in 2009 and 2010, respectively. Looking at large insurers’ half-year results, it’s hard not to agree with Swiss Re’s analysis 📰 Reuters

Coverager released its mid-year Insurtech Insights. Coverager highlights 7 big trends emerging in 2021, namely: the increased interest from insurers in electric vehicles, industrial IoT, the rise of pet insurance, the increased interest in creating home ecosystems beyond insurance, the move to greater fairness in (usage-based car) insurance, embedded insurance, and cyber security/insurance 📰 Coverager

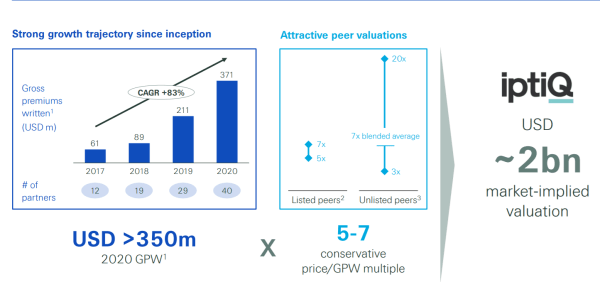

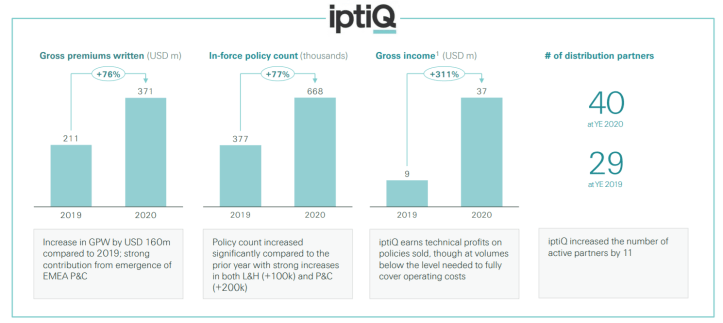

A really interesting read on Swiss Re’s API-led B2B2C insurance unit, iptiQ, and its growing momentum on the market. iptiQ crossed 500,000 customers with 40 partners in 5 markets. Its growth trajectory pegs its market-implied valuation at $2 billion. Growing from 12 to 40 partners over 3 years, iptiQ has consistent, impressive results to show. In-force policies increased significantly y-o-y with increases in L&H and P&C. Another proof that embedded insurance is the future of insurance? 📰 Daily Fintech.

TechCrunch wrote extensively about publicly traded Insurtechs and their valuations, asking whether we should worry about those valuations. It concludes that companies like Metromile or Root Insurance are down on the stock market, with Lemonade being a sort of outlyer with gains compared to its IPO price. TechCrunch also argues that markets have repriced negatively Insurtechs in the last quarters, but that most public neo-insurance companies couldn’t care less: they remain cash rish and market-sentiment poor.

Should we be worried about Insurtech valuations? 📰 TechCrunch

A lot of cash and little love: An insurtech story 📰 TechCrunch (Extra members only)

Great read from VC firm Accel on the future of Insurtechs. Acknowledging the explosion of Insurtech funding in the last 4 years, especially in Europe, Accel makes 5 predictions for Insurtechs:

The verticalization of insurance: the authors believe that new comers, especially MGAs, will continue to specialize in certain verticals and ecosystems, like Luko in home or Ethos in life. I’m not fully convinced by that one, and believe that while some Insurtechs may first go deep into one vertical, the need to diversify and tackle other verticals and business segments arises quickly. Look at Lemonade, which started with renters insurance before expanding to homeowners, pet, life and now car insurance.

Rise of SMB insurance across Europe: taking stock of the successes of Next Insurance and Embroker in the US, the authors predict that new Insurtechs will rise in Europe to serve SMBs. Could not agree more with that prediction!

Embedded insurance everywhere: agreed as well with that prediction, but I’m still hesitant as to when embedded insurance distribution could become widespread. Still waiting for big use cases which I don’t necessarily see as of now.

Insurtech goes further down the stack: after disrupting distribution and customer experience, Insurtechs will move further down the tech stack and help insurers transform.

Europe to see its first $B+ insurtech exit in 2022: agree with this one too! While the US has seen many Insurtech exits in the past two years (Lemonade, Oscar, Hippo, Clover, Metromile, Root), it’s not yet been the case in Europe.

Prepared Minds: the Insurtech landscape and five predictions for the future 📰 Accel